In other words, fixed costs are not dependent on your business’s productivity. Furthermore, an increase in the contribution margin increases the amount of profit as well. To cover the company’s fixed cost, this portion of the revenue is available. After all fixed costs have been covered, this provides an operating profit. The contribution margin shows how much additional revenue is generated by making each additional unit of a product after the company has reached the breakeven point. In other words, it measures how much money each additional sale “contributes” to the company’s total profits.

How Business Leaders Interpret Cost Behavior and Contribution Margin

For instance, increasing production can spread fixed costs over more units, potentially lowering the cost per unit and boosting profit margins. However, this strategy only works within what financial analysts call the “relevant range” of production levels where these cost relationships hold true. For the month of April, sales from the Blue Jay Model contributed \(\$36,000\) toward fixed costs. In fact, we can create a specialized income statement called a contribution margin income statement to determine how changes in sales volume impact the bottom line. The Contribution Margin Ratio is a measure of profitability that indicates how much each sales dollar contributes to covering fixed costs and producing profits. It is calculated by dividing the contribution margin per unit by the selling price per unit.

Step-by-Step Guide to Calculating Contribution Margin

Contribution margin analysis is the gain or profit that the company generates from the sale of one unit of goods or services after deducting the variable cost of production from it. The calculation assesses how the growth in sales and profits are how to prepare a cash flow statement model that balances linked to each other in a business. The first step to calculate the contribution margin is to determine the net sales of your business. Net sales refer to the total revenue your business generates as a result of selling its goods or services.

Get in Touch With a Financial Advisor

- Because contribution margin doesn’t take into account fixed costs.

- The balance between fixed and variable costs carries significant weight in strategic planning.

- Ultimately, gross profit margin is a measure of the overall company’s profitability rather than an analysis of an individual product’s profitability.

- Let’s say we have a company that produces 100,000 units of a product, sells them at $12 per unit, and has a variable costs of $8 per unit.

- The fixed costs for a contribution margin equation become a smaller percentage of each unit’s cost as you make or sell more of those units.

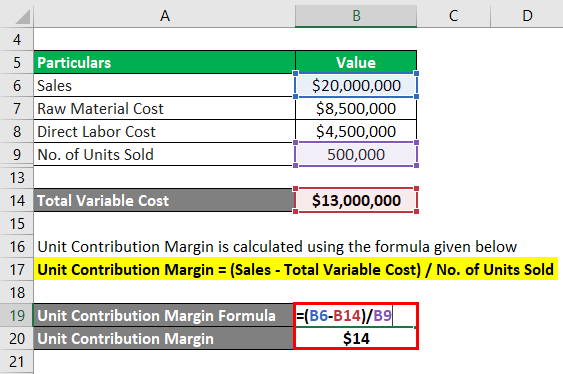

To calculate the contribution margin, we must deduct the variable cost per unit from the price per unit. Watch this video from Investopedia reviewing the concept of contribution margin to learn more. Keep in mind that contribution margin per sale first contributes to meeting fixed costs and then to profit.

To Ensure One Vote Per Person, Please Include the Following Info

For instance, a beverage company may have 15 different products but the bulk of its profits may come from one specific beverage. Where C is the contribution margin, R is the total revenue, and V represents variable costs. You pay fixed expenses regardless of how much you produce or sell. It includes the rent for your building, property taxes, the cost of buying machinery and other assets, and insurance costs. Whether you sell millions of your products or 10s of your products, these expenses remain the same. For this section of the exercise, the key takeaway is that the CM requires matching the revenue from the sale of a specific product line, along with coinciding variable costs for that particular product.

Variable cost

Fixed and variable costs are expenses your company accrues from operating the business. In effect, the process can be more difficult in comparison to a quick calculation of gross profit and the gross margin using the income statement, yet is worthwhile in terms of deriving product-level insights. On the other hand, the gross margin metric is a profitability measure that is inclusive of all products and services offered by the company. The contribution margin (CM) is the profit generated once variable costs have been deducted from revenue. Investors and analysts use the contribution margin to evaluate how efficient the company is at making profits. For example, analysts can calculate the margin per unit sold and use forecast estimates for the upcoming year to calculate the forecasted profit of the company.

Other reasons include being a leader in the use of innovation and improving efficiencies. If a company uses the latest technology, such as online ordering and delivery, this may help the company attract a new type of customer or create loyalty with longstanding customers. In addition, although fixed costs are riskier because they exist regardless of the sales level, once those fixed costs are met, profits grow. All of these new trends result in changes in the composition of fixed and variable costs for a company and it is this composition that helps determine a company’s profit. The difference between fixed and variable costs has to do with their correlation to the production levels of a company.

Business owners, finance teams, and accountants may rely on contribution margins to make a variety of business decisions. For example, companies can determine which products are profitable and which should be discontinued by understanding the contribution margins for each product line. Also, this margin is an important factor in price setting — the contribution margin needs to be high enough to cover fixed expenses and ideally high enough to generate profits. You might wonder why a company would trade variable costs for fixed costs. One reason might be to meet company goals, such as gaining market share.

In other words, your contribution margin increases with the sale of each of your products. Remember, that the contribution margin remains unchanged on a per-unit basis. Whereas, your net profit may change with the change in the level of output. For information pertaining to the registration status of 11 Financial, please contact the state securities regulators for those states in which 11 Financial maintains a registration filing.

The contribution margin represents how much revenue remains after all variable costs have been paid. It is the amount of income available for contributing to fixed costs and profit and is the foundation of a company’s break-even analysis. So, when you subtract your variable costs (lemons, sugar, and water) from your revenue (money from selling lemonade), you get your contribution margin.