Chartered accountant Michael Brown is the founder and CEO of Double Entry Bookkeeping. He has worked as an accountant and consultant for more than 25 years and has built financial models for all types of industries. He has been the CFO or controller of both small and medium sized companies and has sales journal accounting run small businesses of his own.

Recording entries in sales journal

- The sales journal concept is mostly confined to manual accounting systems; it is not always used in computerized accounting systems, where there is less need for subsidiary-level journals.

- This account is for deductions from revenue that result from returns or allowances.

- There are also accounts that have to do with liabilities that must be modified.

- A sales journal entry is a sale entry made in the sales journal when a customer purchases a product.

- A sale made in cash would instead be recorded in the cash receipts journal.

- Cost of goods sold is debited for the price the company paid for the inventory and the inventory account is credited for the same price.

While all companies maintain a single journal for bookkeeping records, some companies like to divide journals into multiple types which makes it easy to track down financial records. Some companies would have multiple sale journals for different types of products. These companies would keep multiple sales journals to track the sales of each product. The sales, their dates, and prices are all listed in chronological order. Sometimes, a specific identification number would also be added to track the product. This specific identification also helps track the inventory.

Cash Sales Journal Entry

A comprehensive ledger containing all of a company’s financial accounts. The idea behind this is related to getting rid of on-hand inventory. When you sell it, you reduce the liabilities you have with inventory. However, it also increases the total cost of goods sold for your business. The company also has a tracking identification number for the LED light.

Q: Are accounts payable affected by sales?

So you give them a discount of 20% to make up for the inconvenience, making the final sale price $40. We’ll also assume a 10% sales tax and a $15 cost of goods sold. This can be a bit confusing if you’re not an accountant, but you can use this handy cheat sheet to easily remember how the sale journal entry accounts are affected. Debits and credits work differently based on what type of account they are.

Post reference entries

An increase to your sales tax liability account is necessary. When you make a sale, a collection of sales tax also takes place, hence the increase to the liability account. In modem age, the introduction of cash receipts journal is in practice in medium and large size business organizations. So, at the time of posting in the ledger, its dual aspects are to be completed.

What Is a Sales Journal Entry?

- When you make a sale, a collection of sales tax also takes place, hence the increase to the liability account.

- Cash sales are not recorded in the sales journal; rather, they are recorded in another special journal known as the cash receipts journal.

- Sales invoices are the primary inputs into the sales journal.

- When recording sales, you’ll make journal entries using cash, accounts receivable, revenue from sales, cost of goods sold, inventory, and sales tax payable accounts.

- Here’s how Little Electrode, Inc. would record this sales journal entry.

- To create a journal entry in your general ledger or for a sale, take the following steps.

Now, there is software that automatically enters the day, time, and even the name of the goods sold. This software also allows the inventory to be automatically updated when a specific good is running low on inventory, by automatically ordering that particular good from the supplier. At the end of the month, the amount column in the journal is totaled.

This total is then posted as a debit in the accounts receivable control account and as a credit to the general ledger sales account. The example below also shows how postings are made normal balance from the sales journal to both the subsidiary and general ledger accounts. Each individual sale is posted to its appropriate subsidiary account. The sales journal, sometimes called the credit sales journal, is used to record all sales made on account.

- Sales are credit journal entries, but they have to be balanced by debit entries to other accounts.

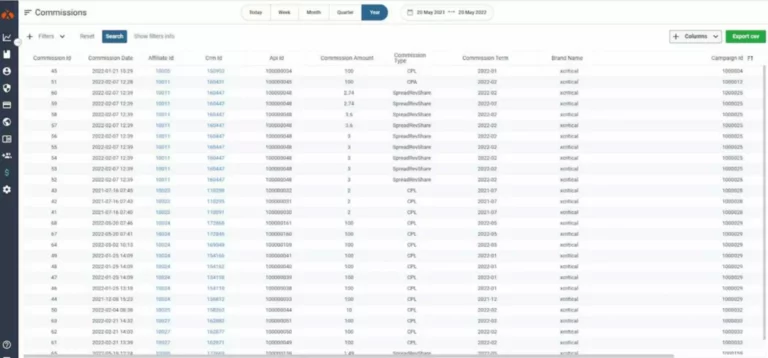

- The transaction number, account number, customer name, invoice number, and sales amount are typically stored in the sales journal for each sale transaction.

- A Sales Journal, also known as the Sales Day Book, is a specialized accounting journal used to record all credit sales of merchandise.

- A sales journal entry is a journal entry in the sales journal to record a credit sale of inventory.

- Under the double-entry system, there are mainly 7 different types of journal in accounting.

The sales journal (also known as the sales book or sales day book) is a special journal used to record all credit sales. Every transaction that is entered in this journal essentially results in a debit to the accounts receivable account and a credit to the sales account. Cash sales are not recorded in the sales journal; rather, they are recorded in another special journal known as the cash receipts journal.

Налог с продаж в США или что такое Sales Tax

Therefore, the journal, wherein the transactions which cannot be directly recorded in a particular journal are recorded, is called journal proper. Balancing ledger accounts is not generally determined or shown until the end of the year, because posting in these accounts may be needed throughout the whole year. It is difficult to find out effects and information relating to the transaction if all the transactions law firm chart of accounts are recorded in a single journal. Recording of all transactions in one general journal is a time consuming, laborious and troublesome task.